LIFO often creates material long-term tax deferral/savings: Not just a one-time tax benefit or timing difference between book & tax such as straight-line vs. accelerated depreciation

During periods of rising costs, LIFO:

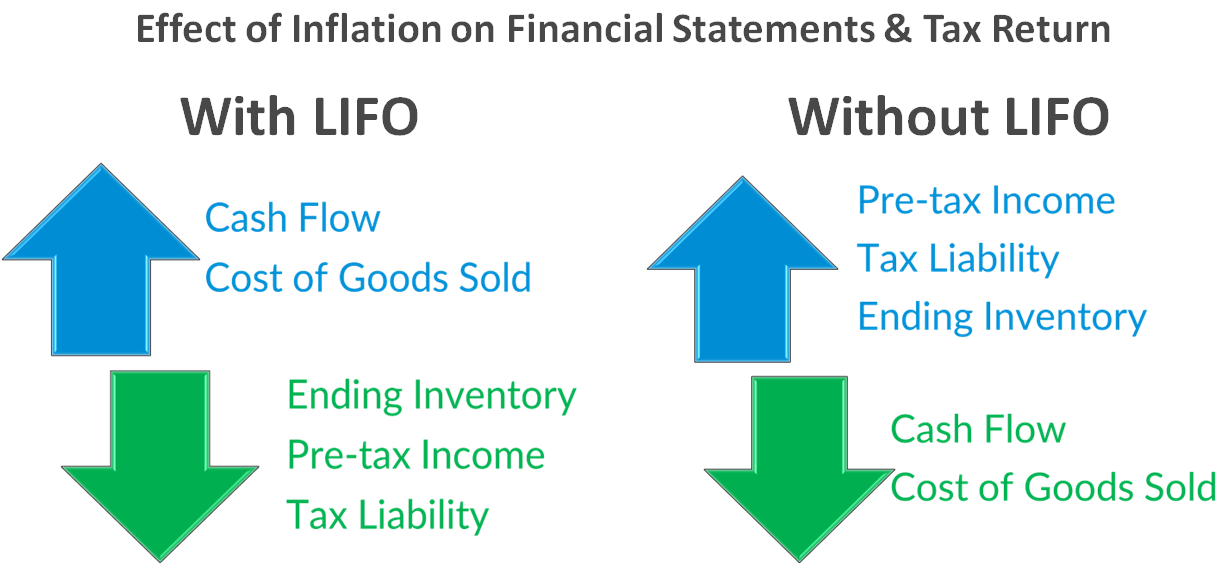

Provides more after-tax free cash flow than non-LIFO methods when there’s inflation

Ensures taxes aren’t paid on goods that have been purchased, but have yet to be sold

Improves ability to replenish & maintain an adequate level of inventory

Some consider LIFO to act as a tax deferral tool that can be thought of as an interest-free loan

Others believe that LIFO essentially acts as a permanent form of tax savings if a company is profitable, satisfies the going concern assumption & intends to stay on LIFO in perpetuity

Tax Court opinion regarding LIFO (see Amity Leather vs. Commissioner): The theory behind LIFO is that income may be more accurately determined by matching current costs against current revenues, thereby eliminating from earnings any artificial profits resulting from inflationary increases in inventory costs. At the heart of the LIFO method is the principle that income is more clearly reflected by matching current costs with current revenues.

Preferable accounting method

LIFO is an accounting method permissible under GAAP, not just a tax incentive

During periods of rising costs, income is most clearly reflected by matching current costs with current revenues

Provides a more conservative measure of income compared to non-LIFO methods during periods of rising costs.

Acts as a mechanism that’s similar in nature to nominal to real GDP adjustment

When there’s inflation, portion of ending inventory balance is transferred to cost of goods sold to normalize reported income & tax liability

Isn’t a tax loophole that always provides a benefit since deflation causes LIFO recapture or additional income to be recognized

Misconception #1: The following burdens & costs outweigh the benefits of LIFO:

Management, cost accounting & purchasing/sales functions & responsibilities will be complicated by using LIFO

Wholesale changes must be made to accounting system since item costs & the physical flow of goods must be tracked on a LIFO basis

Clarifications

Under the dollar-value method, the LIFO value of inventory is determined outside of the accounting system & a top-side accounting entry is recorded to adjust ending inventory from cost to LIFO & accrue the change in the LIFO reserve

Under dollar-value LIFO, item costs remain being tracked the same way they did prior to electing LIFO & requires no changes to the accounting system other than adding a contra-inventory subledger account called the LIFO reserve

Misconception #2

Employee compensation & bonuses will be complicated from using LIFO

Clarification: Internal management reports can be presented on a non-LIFO basis as long as they’re only being used internally

Misconception #3: Tax savings from LIFO will be minimal because of:

High inventory turnover or new item rates

Just in time inventory or lean accounting practices

Clarifications

Under the dollar-value method, the inflation rate used to calculate the LIFO reserve change is based on a 12 month comparison of current vs. prior year’s item/unit costs extended by quantities on hand in ending inventory regardless of the turnover ratio

External indexes reconstruct inflation on new items, which ensures the same amount of inflation is applied to new & preexisting items

Manufacturers will always have raw materials & WIP; wholesalers/distributors & retailers still must maintain adequate base stock

Misconception #4: Internal costs must be used to measure LIFO inflation

Clarification: External indexes such as the BLS CPI/PPI can be used to measure inflation, thereby minimizing reliance on accounting information systems

Accounting system continues tracking inventory costs the same way before and after LIFO is adopted, meaning LIFO is never applied at the item level (unit costs are never converted to LIFO)

LIFO reserve contra inventory account added to subledger to enable a top-level adjustment to be annually recorded to account for the difference between inventory at cost in accounting system (FIFO, average cost etc.) & inventory at LIFO

LIFO side calculation made outside of accounting system to determine the LIFO inventory balance and CY vs. PY LIFO reserve change & journal entry recorded to adjust cost of goods sold & CY vs. PY LIFO reserve change

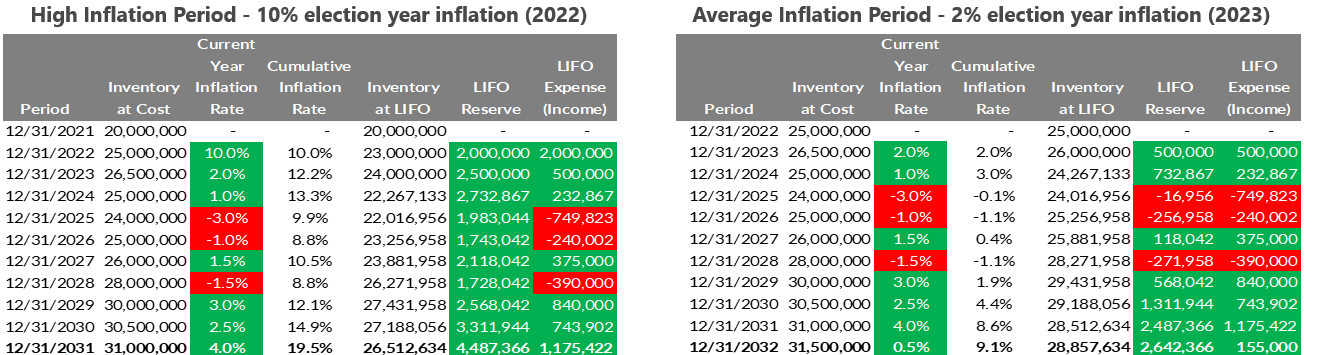

Companies with high inflation frequency and/or high historical average inflation rates are often ideal LIFO candidates

Companies with a combination of high inflation frequency and historical average inflation rates are the best LIFO candidates

High Inflation frequency: Common profiles include wholesalers & retailers. Includes some of the most predominant users of LIFO, such as auto dealers & supermarkets.

Pros

LIFO reserve essentially grows in perpetuity & acts as a tax savings annuity since there’s rarely (if ever) deflation for industries with highest inflation frequency

Often shielded from volatility of raw materials commodities, meaning LIFO recapture rarely if ever happens, and when it does, it’s usually immaterial

Industries with the highest inflation frequency tend to stay on LIFO the longest

Attractive for nearly all risk appetite profiles since there’s minimal downside

Cons

Tend to have lower historical inflation rates & long-term tax benefits from LIFO compared to industries with lower inflation frequency

May be less appealing to companies requiring material short-term benefits if the historical average inflation rate is on the lower end of the spectrum

High historical average inflation rates & tax benefits: Common profiles include manufacturers and industries with volatile raw materials such as chemicals, lumber & steel wholesalers (metal sheet/strip/coil, bars/shapes/pipes etc.)

Pros

Tax benefits of LIFO are highly likely to far outweigh administrative burdens/ costs for industries with the highest historical average inflation rates

Largest long-term tax benefits from LIFO are typically found in these industries

Massive LIFO reserves can be built in a short amount of time

Attractive to companies with high risk appetite

Cons

Tend to have lower historical inflation frequency, which results in a higher probability of taxable income being created from LIFO

Not ideal for companies with low risk appetite if there is low inflation frequency since material LIFO reserve recapture is a real possibility every so often

Industries with the highest historical average inflation rates and low inflation frequency tend to go off LIFO more frequently

Company-specific metrics such as historical inflation frequency and average annual inflation rates should be included in the LIFO due diligence process to ensure each company’s risk/reward profile matches or aligns with the potential short/long term benefits and costs of LIFO

Good LIFO Candidate: LIFOPro has developed a proprietary scoring system to identify good candidates, which requires for the following criteria to be met –

High inflation frequency: Must have inflation in more than half of the last 20 years (11 or more). Best LIFO candidates have high inflation frequency because the more often inflation is expected to occur, the higher the likelihood that LIFO acts as annuity & the lower the likelihood of deflation/LIFO recapture

Historical average annual inflation rate of 1% or greater: Ensures an adequate amount of long-term inflation exists for the benefits of LIFO to far outweigh the cost. Most predominant users of LIFO such as auto dealers & supermarkets have a 1% – 2% long-term average inflation rate.

At least $2M – $5M of inventory: Appropriate range dependent on historical inflation rate, tax rate & company’s perceived value of LIFO tax benefits

Good 2023 LIFO Election Candidate: Must meet the good LIFO candidate criteria listed above & have an election year inflation rate that’s greater than or equal to the historical average annual inflation rate

Face of the annual or year end income statement must present income, profit or loss using the LIFO method beginning no later than the year that LIFO is adopted for tax purposes

Once LIFO has been elected for tax purposes, income, profit or loss must be computed using LIFO on the face of all subsequent annual financial statements (unless LIFO is terminated for tax purposes)

Non-LIFO Disclosures

The following non-LIFO disclosures and information are allowed to be made within the financial reports while maintaining LIFO conformity compliance (see IRS Regs. §1.472-2(e)):

Reporting cost of goods sold or operating profit on a non-LIFO basis and reporting LIFO as a nonoperating item in the primary income statement – Companies are allowed to present cost of goods sold and operating profit on a non-LIFO basis without violating the LIFO conformity rule as long as there’s an adjustment so that ending net income is calculated on a LIFO basis. This can be accomplished by including the LIFO adjustment as a nonoperating item on the income statement (supplemental schedule of nonoperating items could be included if there are multiple nonoperating items)

Supplemental and explanatory information using a non-LIFO method – Includes anything other than the primary presentation of the income statement, which includes the following:

Notes to the income statement

Appendices & supplements to the income statement

Other reports included in the financial reports, such as:

Management’s discussion and analysis

Statement of changes in financial position

Letters to shareholders, partners or other stakeholders

Summary of key figures

Inventory asset value disclosures using a non-LIFO method, including balance sheet disclosures

Internal Management & Interim Reports

Internal Management Reports – The use of a non-LIFO method is allowed on all portions of internal management reports as long as the reports will not be issued or released to parties outside of the organization. Examples include earnings projections, budgets, sales and sales forecasts.

Interim reports – If issued in accordance with GAAP, same LIFO disclosure rules described above apply. If not issued in accordance with GAAP, then interim reports are not required to be presented on a LIFO basis (exception is a series of interim reports that can be used to ascertain income, profit & loss by combining those reports)

Switch to IPIC method (using Bureau of Labor Statistics Consumer/Producer Price Index)

Tax deferral maximization: Often creates more inflation than actual internal product costs or internal index inflation for the following reasons:

BLS PPI inflation will be greater than internal index inflation on goods that were imported or purchased for resale products sourced from abroad because BLS PPI only measures U.S. or domestic production & domestically produced goods inflation rates have historically been materially higher than imported goods

When the IPIC method is used, new items are given preexisting item inflation since BLS only measures price changes on preexisting items (or they reconstruct the cost on any newly-introduced item). With internal indexes, new items’ prior year costs are often set to equal to its current year cost since reconstruction is often burdensome/subjective & IRS Regs. prohibit new items from being excluded from the inflation calculation. As a result, during periods of inflation, new items will reduce the overall current year inflation rate when internal indexes are used. This becomes more pronounced when there’s high item turnover and/or high inflation.

Much quicker, simpler means of performing interim estimates than internal indexes

Minimize IRS scrutiny upon audit or reduce audit risk

IPIC method is IRS safe harbor method, which affords taxpayers less scrutiny from IRS upon audit compared to taxpayers using internal indexes since inflation calculation relies on external government indexes & internal indexes rely on the taxpayer’s accounting records/systems

Switch to IPIC method from internal indexes to IPIC method provides audit protection from prior period calculation errors

IPIC method can simplify inflation calculation for manufacturers because:

Reduces reliance on accounting information systems & appropriate allocation of item cost components such as materials, labor & overhead since inflation is measured using BLS PPI, not current & prior/base period item/unit costs

Inflation for WIP inventories are calculated by assigning the applicable finished goods PPI code to the WIP items

IPIC method can reduce volatility because BLS surveys thousands of producers & eliminates extreme cost fluctuations that could occur within any single company

Automatic approval to change to IPIC method & is applied on a cutoff basis

Affords audit protection from LIFO reserve overstatements since change is applied beginning in year of change & built from pre-change LIFO reserve

Only means of automatically changing from double-extension to link-chain (double-extension = current vs. base year cost comparison; link-chain = current vs. prior year cost comparison; advanced approval change to switch from double-extension to link-chain internal index)

Auto dealers can use alternative LIFO method (ALM) using actual invoice costs or IPIC method using Bureau of Labor Statistics Consumer/Producer Price Indexes (BLS CPI/PPI)

Prior to 2020, majority of auto dealers used ALM because it created more tax benefits than IPIC method

IPIC method has grown exponentially in popularity beginning in 2020 primarily because of materially higher tax benefits

Secondary benefit of IPIC method is minimal administrative costs, simplest means for performing interim estimates & more flexibility in terms of meeting LIFO conformity financial reporting requirements when compared to ALM

Alternative LIFO method (ALM)

Measures inflation based on comparing current & prior period’s invoice costs

Item definition is specific to each vehicle/VIN, meaning inflation must be calculated for each vehicle

Inflation calculation is materially more burdensome since invoice costs must be compared on a vehicle-by-vehicle basis

Specific goods (“unit LIFO”): LIFO value of inventory is accounted for at the item level. Unit costs & the physical flow of goods are tracked on a LIFO basis within accounting system

Dollar-value: Under this method, the LIFO value is accounted for as a top-side adjustment rather than at the item level. Unit costs & the physical flow of goods are tracked at actual cost (FIFO, average cost or specific ID) or standard cost. Side computation made outside of accounting system to calculate inflation, layers (decrements), inventory @ LIFO, LIFO reserve & LIFO expense (income)

Best practice: Use dollar-value LIFO because it avoids many undesirable characteristics of LIFO & offers materially higher long-term tax benefits when compared to unit LIFO

LIFO index computation timeframe selection

Link-chain: Current quantities are extended against current & prior period item/unit costs to calculate current year inflation index (one year measurement period)

Double-extension: Current quantities are extended against current & base period unit costs to calculate current year cumulative index (all years on LIFO measurement period)

Best practice: Use Link-chain LIFO because it’s absent of the inherent flaws built into double-extension method & link-chain precludes the need to reconstruct base year costs for new items

Inflation measurement source

Internal indexes: Current year inflation index measured using actual costs paid/incurred to acquire/procure the goods

External indexes: aka Inventory Price Index Computation or IPIC method. Bureau of Labor Statistics Consumer/Producer Price Indexes assigned to goods to calculate current year inflation index

Best practice: Common to use the method that’ll provide the most favorable tax position (inflation), but ultimately varies by industry, product mix & many other company-specific considerations

Current-year cost & layer valuation method

Latest acquisitions (FIFO)

12-month moving average or rolling-average cost (aka weighted average cost)

Earliest acquisitions

Specific identification

Any other method that’s clearly reflective of income

Best practice: For first-time elections, use the same method employed by accounting system to track item costs prior to electing LIFO to prevent wholesale changes to accounting system or IT burden associated with measuring multiple methods

Pooling method

Resellers (retailers & wholesalers/distributors)

By line or class of goods

Natural business unit can be used in certain cases

Manufacturers/producers

Natural business units (separate pool required for manufactured vs. purchased for resale goods)

Raw materials content

Multiple pools

IPIC LIFO method users

IPIC Pooling method: pools established for each BLS major group assigned 5% or more of the total inventory balance at cost

Any non-IPIC pooling method listed above that matches your industry type ( i.e., manufacturers using IPIC method could use natural business unit pooling method)

Best practice: Utilize the method expected to create/require the least amount of LIFO pools to minimize likelihood of LIFO recapture caused by inventory liquidations

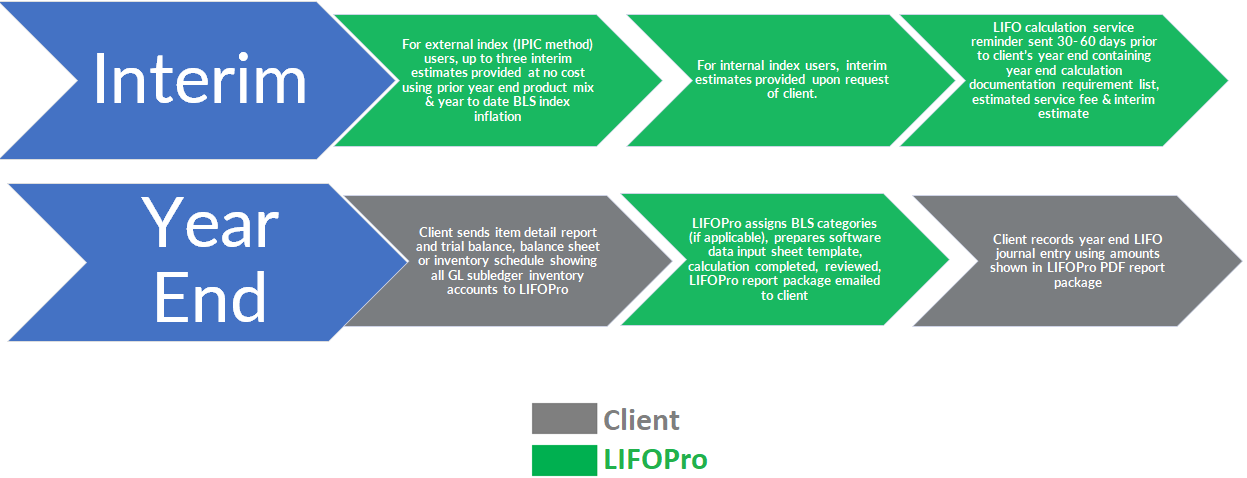

Companies perform interim LIFO estimates for a wide array of reasons, including:

Financial reporting compliance – Under Generally Accepted Accounting Principles, an estimate for the interim cost of sales is required for interim reporting purposes. Because of this, companies issuing GAAP financial statements include an estimated LIFO adjustment in their interim reports. Also, some companies are required by their lenders or suppliers to issue interim financial reports, and as a result, companies may also be required to include an estimated LIFO adjustment in their interim estimates.

Tax compliance – Although IRS Regs. don’t require for interim estimates to be performed (tax law defines LIFO as an annual calculation), many companies perform interim estimates to incorporate the LIFO effect into their quarterly estimated tax payments

Forecasting and planning – Many companies perform at least one interim LIFO estimate in order to properly forecast and plan the estimated LIFO effect on their bottom line. An added benefit of doing so is to smooth out the effect of the estimated LIFO reserve change over the course of the year as opposed to booking a single LIFO adjustment at year end. An added benefit of forecasting & planning is that one can avoid material or unexpected surprises from LIFO at year end. These types of estimates come in many shapes and forms in terms of frequency, including mid-year estimates, ones made towards the end of the year, and some even perform estimates on a monthly basis (monthly estimates are the least common interim estimate frequency)

Maximize the LIFO reserve increase (or minimize the decrease) – When there’s inflation, a minimum “Current-year cost” balance is required to avoid what is known as layer erosion effect LIFO income (Current-year cost can be thought of as inventory at cost i.e. FIFO or average cost). If the Current-year cost balance is below the minimum required amount, layer erosion effect LIFO income can erode or completely wipe out the LIFO expense created by inflation for that period (or in some cases, a net LIFO reserve decrease can occur from substantial layer erosion income). Because of this, some companies will plan their year end purchases to achieve the most desirable LIFO results to minimize the effects of layer-erosion LIFO income.

Companies that don’t issue interim financial reports are not required to perform interim LIFO estimates

Companies that issue non-GAAP interim reports are also not required to perform interim LIFO estimates

LIFOPro offers solutions to make quickly obtain accurate interim LIFO estimates

Up to 3 interim estimates are included in LIFOPro’s outsourcing engagements for companies using the IPIC method

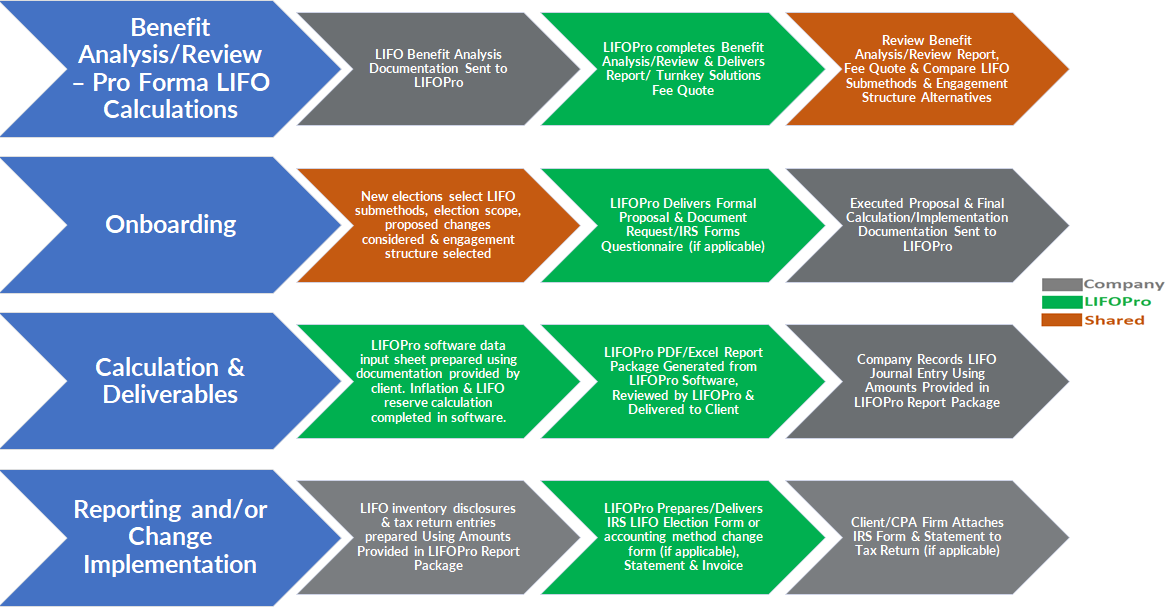

Companies not on LIFO: LIFO Election Benefit Analysis

Comprehensive LIFO election case study packaged in the form of a PDF report containing the following:

Election year estimated tax LIFO benefits, including comparisons between internal vs. external inflation measurement source

20 year pro forma IPIC LIFO calculation using Bureau of Labor Statistics Consumer/Producer Price Indexes to determine inflation frequency, long-term historical average annual inflation rate & whether a company is a good LIFO candidate

Election recommendations including which submethods should be used

How LIFO Works appendix covering all the essentials

LIFOPro also provides turnkey outsourcing solution fee quote showing election year & recurring costs

Inflation calculation can be very complex when performed in spreadsheets

Important steps may be overlooked or left out altogether when manually performed in-house, such as:

Using too few BLS categories increases IRS audit risk & using the wrong BLS categories causes distorted inflation calculation

Using 10% method BLS category assignment approach where less-detailed BLS categories are used, but using a non 10% category inflation index approach (impermissible per IRS Regs.)

Uniform BLS category assignment to new items to ensure the same BLS indexes are applied to similar new vs. preexisting items

Including new items in calculation ensure compliance or reconstructing new item cost to avoid inflation dilution that’d otherwise occur

Performing inflation calculation reasonableness testing, setting criteria for identifying inflation outliers & establishing standard procedures for handling outliers

Calculating layers & decrements can be complex because it’s unknown whether there’ll be an increment or decrement in any given year & different math steps are required to calculate an increment vs. decrement(s)

Calculation errors become more inevitable the longer you’ve been on LIFO as decades worth of LIFO layers accumulate

Outsourced calculations or those made in-house WITH software

Make being on LIFO as simple as possible with outsourcing & minimize time spent on LIFO in-house with software

Reduces control & detection risk since all aspects of the calculation is automated using LIFOPro software

Simplifies audit procedures by providing comprehensive, user-friendly documentation

CPA firms & companies can rely on LIFOPro to serve as their LIFO subject matter expert rather than having to develop & maintain in-house expertise

All tasks related to LIFO calculation & documentation outsourced to & managed by LIFOPro, including:

BLS category assignments (if applicable)

Inflation calculation, including new item cost reconstruction, exceptions & outlier analysis

LIFO reserve calculation

LIFO calculation documentation & storage

LIFOPro report package preparation

All clients receive LIFOPro report package electronically containing comprehensive calculation documentation, including summary amounts required to record LIFO-related accounting entries & tax return line items

Clients using external indexes (IPIC method) receive up to three interim estimates at no additional cost (using prior year product mix & year to date BLS inflation rates)

Flexible engagement structures to include supplemental services

Includes up to 40 hours of audit support

Benefits

Make being on LIFO as simple as possible

Simplifies audit procedures for companies & auditors by providing them with comprehensive, standardized documentation

Increase transparency & understandability by converting many years worth of files & documentation into a single user-friendly LIFO report package containing comprehensive documentation

Complete LIFO calculation & documentation automation for all dollar-value methodologies (excluding auto dealer alternative LIFO method inflation calculations; auto dealer IPIC LIFO inflation calculation is supported)

Automates all aspects of the LIFO calculation (excluding BLS category assignments), including:

Inflation calculation, including new item cost reconstruction, exceptions & outlier analysis

LIFO reserve calculation

LIFO calculation documentation & storage

Printing and/or saving all LIFOPro reports as PDF or Excel files

Separate stand-alone inflation calculation modules for internal & external (IPIC) indexes & both include a complete range of features & settings

Projections module provides on-demand, unlimited array of next year’s LIFO expense (income) figures

Easily & quickly make interim estimates & ad-hoc projections

Additional benefits for CPA firms include:

Quickly perform LIFO benefit analysis for clients who are good candidates

Quickly confirm/verify LIFO calculation accuracy for audit/review clients

Create a highly profitable recurring revenue center by using the software to do all the LIFO heavy lifting & providing LIFO outsourcing services to clients

LIFO tax benefits are primarily driven by inflation, so the timing of the LIFO election is key which makes it extremely important to incorporate LIFO into year end tax planning and annually ID clients that are good LIFO candidates

Because of this, CPA firms should annually ID clients that are good LIFO candidates as a part of the year end tax planning process to maximize the election year LIFO tax benefits

CPA firms play a key role in advocating for their clients to explore adopting LIFO because NO ONE ELSE WILL!

Due diligence should be performed prior to electing LIFO to weigh risks/rewards, set long-term expectations, ensure compliance, select the most appropriate submethods & maximize tax benefits

LIFO reviews should be periodically performed for companies already on LIFO for the following reasons

Identify errors & compliance issues

Quantify potential audit exposure and learn how certain changes can reduce/eliminate audit risk

Identify opportunities to utilize more optimal methods

LIFOPro’s resources provide CPA firms with all their LIFO needs

Generate or maximize revenues by engaging us directly & reselling our services to clients

Enhance ability to provide LIFO as a tax planning strategy without incurring costs & resources to do so

Place reliance on a LIFO subject matter expert and resource who can also serve as their client’s 3rd party LIFO service provider without having to maintain in-house LIFO expertise

LIFOPro’s offerings provide companies with all their LIFO needs

Companies can make being on LIFO as simple as possible with LIFOPro’s turnkey outsourcing solutions

Companies can minimize time spent in-house on LIFO & guarantee accuracy with our software

Get educated on the Inventory Price Index Computation (IPIC) method, including the origins, advantages & disadvantages, calculation procedures, options & much more!

Learn about LIFO opportunities abound for CPA firms, how to increase the scope of your LIFO offerings & learn how to easily identify good LIFO candidates!

Learn how the IPIC LIFO Method works, find valuable Bureau of Labor Statistics (BLS) links and stay up to date on all changes related to the IPIC Method!

Learn about LIFOPro’s past roles in partnering with companies & CPA firms to deliver great value by finding solutions to the most challenging LIFO issues!

The Inventory Price Index Computation (IPIC) method allows taxpayers to use published external indexes to calculate inflation for the purpose of valuing LIFO inventories.

Supermarkets face LIFO calculation issues unique to the industry. Find out why & answers to how they are dealt with Special Challenges for Supermarkets page.

Why the Double-extension LIFO Index Calculation Method is Unreliable

Facts describing why the double-extension LIFO index calculation method is unreliable and examples proving how this method creates unpredictable results.

Find recent important changes & BLS addition of Table 9 Wherever-provided Services & Construction PPI Indexes & Important Change in PPI Code Structure page.

Find information on CPI Category Changes & Bureau of Labor Statistics Consumer Price Index update information such as new medical commodity codes here!

Learn IRS Regulations Requirements for missing PPI Indexes, procedures for reassigning discontinued PPI Categories at LIFO-PRO’s PPI Category Changes page.

Producer Price Index Usage by Supermarkets to Increase Tax Deferral

Learn how drugs, non-foods & food/beverage indexes cause increase LIFO tax benefits at our PPI Index Usage by Supermarkets to Increase Tax Deferral page.

Switching from the double-extension to link-chain method? Want to achieve higher possible inflation indexes? Learn more at the IPIC LIFO Advantages page.

Request a software trial, LIFO Election Benefit Analysis, Best LIFO Practices Methods Review or cost estimate. All of our requests are complimentary & free of obligation!

Accounting and financial professionals who work with LIFO need to understand the jargon associated with LIFO. Below are a number of LIFO-related terms.

Get answers to who should use the LIFO method, how much LIFO may benefit your company or client & good LIFO candidates by industry & principal business activity along with historical inflation data.